A financial product your users never adopt doesn't grow your revenue, and it doesn't grow ours either. This is by design. Many providers focus primarily on infrastructure, but Unit also invests in tooling designed to help improve end-user adoption. After launching more than 100 embedded finance programs, we've observed common points in the user journey where adoption can slow or drop off. We've built the Ready-to-Launch product to address those points, and our team works with you on the ones that need more hands-on support.

Here's what that looks like in practice.

Before they apply

For many users, an account application is a cold start. They've never seen the product work. They don't know what they're signing up for. Asking them to apply before they've seen any value is asking them to make a decision without enough information.

That's why we built ready-to-use marketing banners, promotional cards, and in-product tiles you can insert directly inside your platform and email flows. They surface your embedded finance product at the moments that matter most. Because we support testing these in sandbox, your team can experiment with placement and messaging before anything goes live.

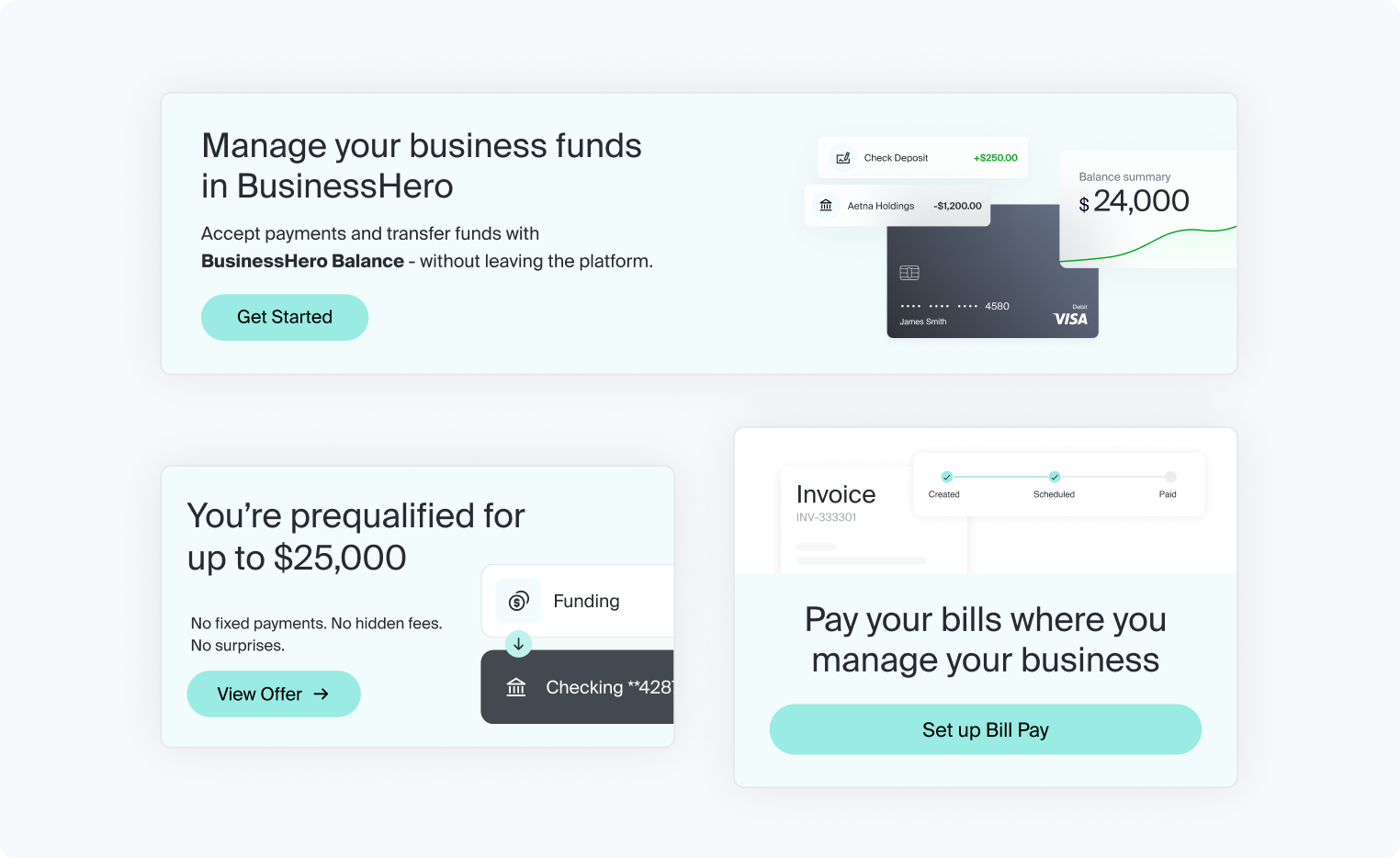

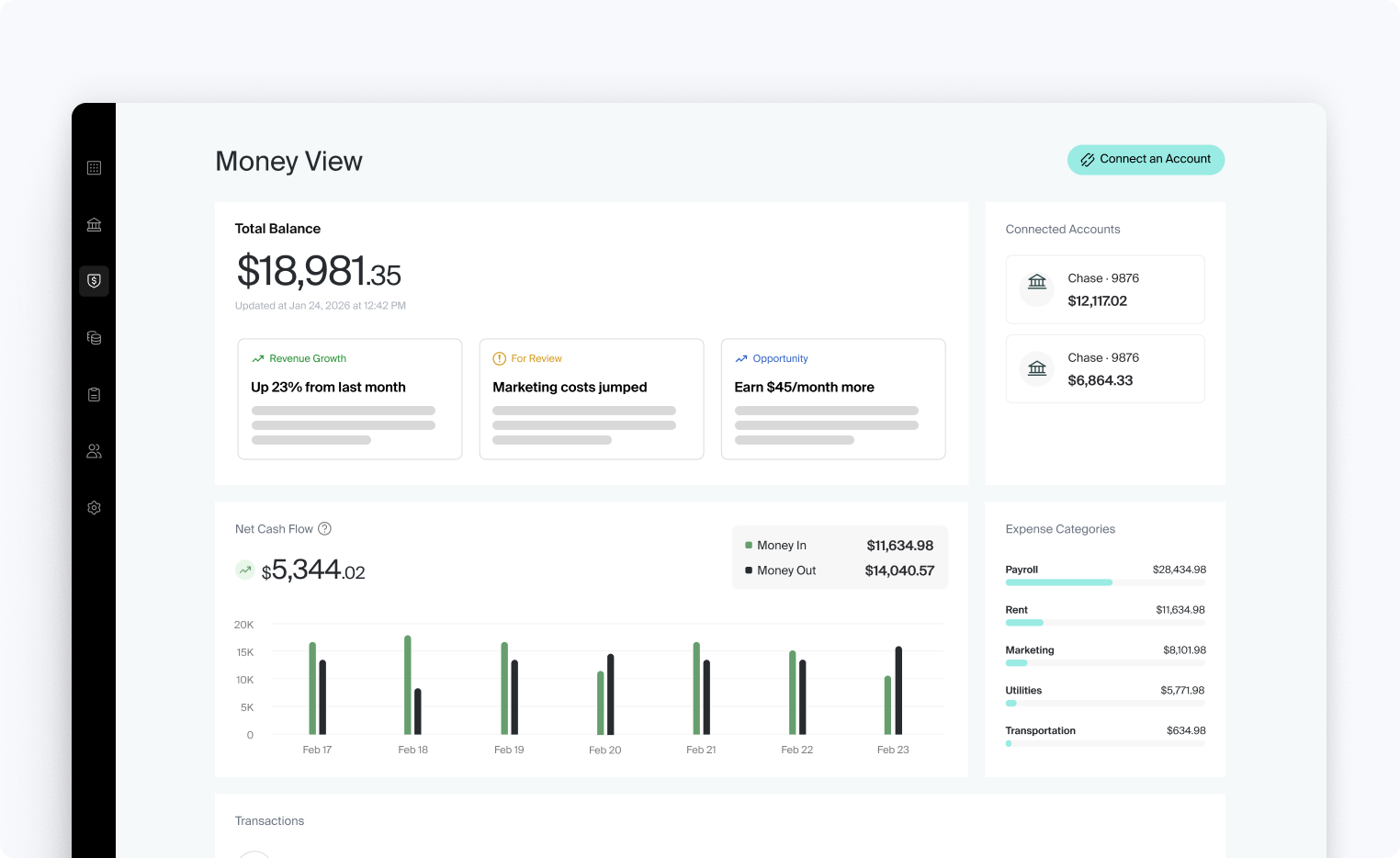

Money View is designed to break that cold-start sequence - asking users to apply before they’ve seen the product work or understood why it matters to them. It's a set of financial insights surfaced inside your platform that show users where their cash is coming from, what bills are upcoming, and where their money is going, using data from accounts held at our partner banks. Users get value before they're asked to complete an onboarding application, and a taste of what's in store once they do. Opening an account or applying for capital becomes the next logical step.

The same principle applies to products like Bill Pay. Most platforms ask users to complete business verification before they've had a chance to understand what they're setting up. Certain Bill Pay functionalities can be accessed before KYB is completed: users can explore workflows, such as uploading bills and adding vendors, before completing verification requirements. Payment initiation requires completed KYB. By the time KYB appears, they already understand what they're building toward.

You can also use rewards to strengthen the value proposition before a user applies. Where available, cash rewards and cash back can be surfaced in the same pre-application touchpoints to give users a clear, immediate reason to engage. Used thoughtfully, these incentives can help turn awareness into application intent by making the benefits of the product more concrete.

During onboarding

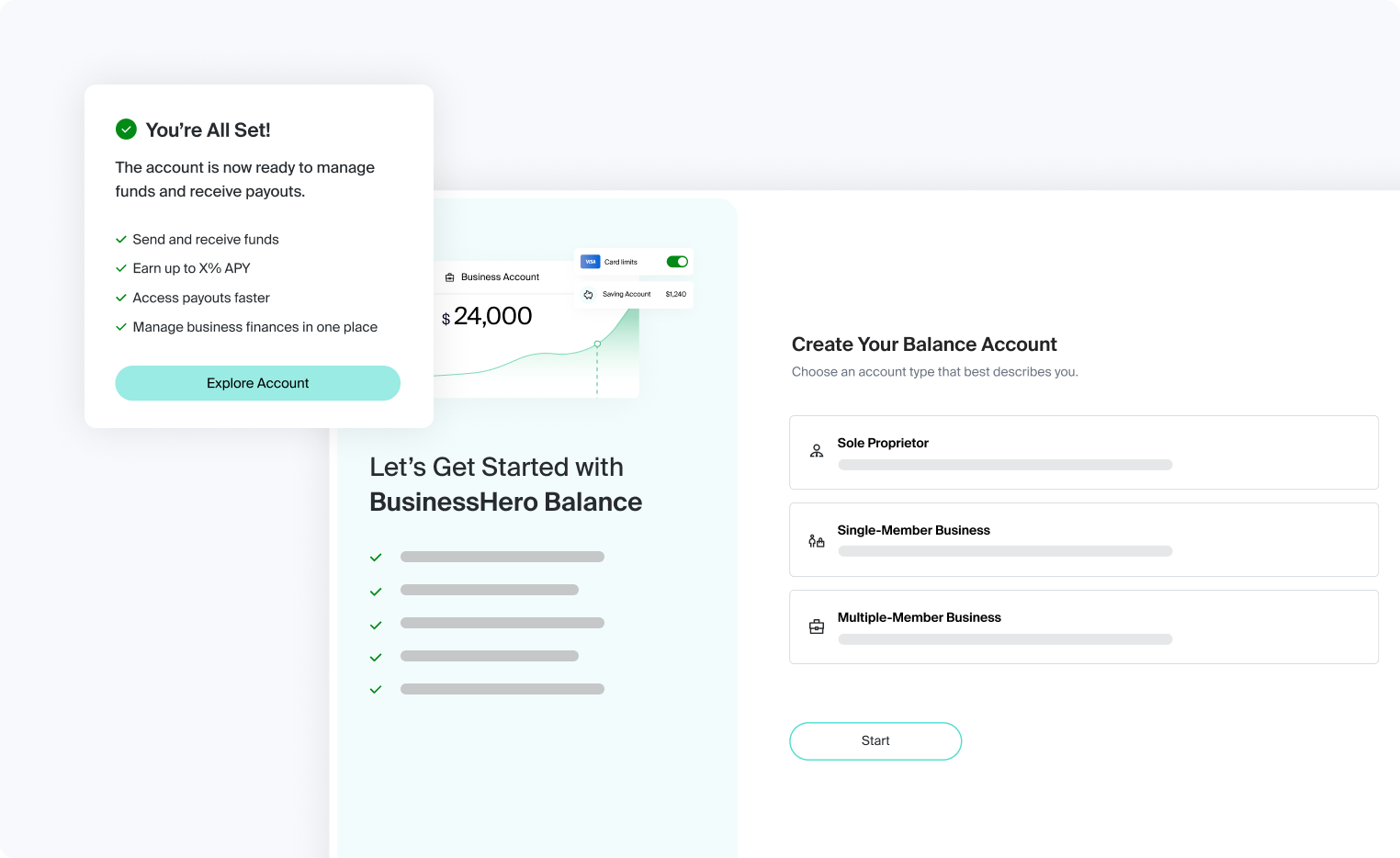

Asking users to complete a separate financial application after they've already set up your product is one of the most reliable ways to lose them. The Ready-to-Launch application form can be embedded so that inside your existing product application flows. Users complete it without being handed off to a separate interface. Further, an AI-powered pre-fill feature populates fields from partner-provided data, so users land on a mostly-filled form instead of a blank one.

Unified Onboarding takes that further: one application covers both your payment processor and Unit products. Your team tracks a single status instead of two moving independently. Document uploads and identity verification happen in-line. And if a user already has a payment processor account, Unified Onboarding links it rather than creating a duplicate.

Partners who launched Unified Onboarding have seen up to 3x improvement in onboarding conversion within days.

After approval

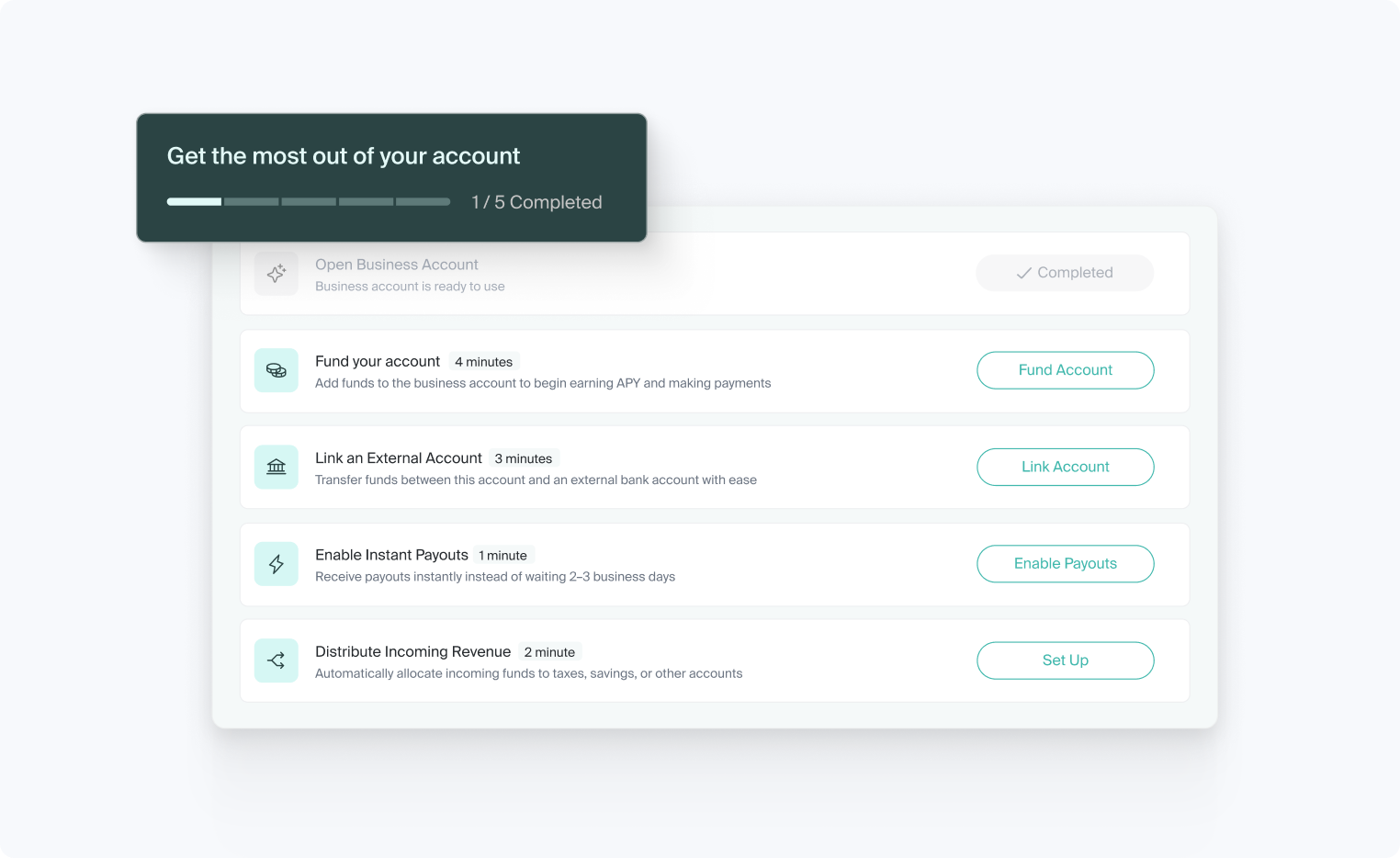

Plenty of approved users never fund their account, never add a vendor, never submit a payment. They may not know which action matters first, or what to do if they get stuck.

The Getting Started module is a post-approval checklist inside your product that surfaces the specific actions that matter, in order. For Bill Pay, that might mean uploading the first bill, adding the first vendor, submitting the first payment. For Banking, it might mean funding the account or setting up the first transfer. For Capital, it might mean reviewing an offer and drawing down funds. Users are presented with a clearer path forward without your team having to build it.

One of the most common Bill Pay blockers is missing vendor payment details. Most platforms hit a wall here: you can't pay a vendor until you have their account and routing number, and getting that information requires chasing them down outside the product. The vendor payment request flow helps streamline that process. Users can schedule bills for payment before they have their vendor's banking details. The vendor receives an email with a secure link to fill in their own information and the payment moves forward without the user ever leaving your platform.

Keeping them engaged

Lifecycle communications for a financial product typically get built after launch, by the platform's engineering and marketing teams, on top of everything else. We built them into the product instead: automated communications can be triggered by user behavior, such as reminders for unfunded accounts, nudges for incomplete applications.

What makes those communications land at the right moment is real-time data. Unit sends webhook events for a broad range of relevant events in your users' bank-powered financial product activity: an application status change, an account opening, a card activation, a transaction posting. Your platform receives those signals instantly, which means you can act on them immediately: update your UI, trigger a workflow, surface a contextual notification, or log the event to your own systems. For construction software, an incoming payment on an invoice can automatically update job costing records in the same platform where the work was managed with no manual reconciliation. The result is a product that responds the way your users expect.

Infrastructure can get you live, but adoption often requires additional tooling, workflows, and engagement strategies. The tools above exist because we've watched enough programs launch, and stall, to know exactly where the work happens after go-live.

If you want to build money products your customers will actually use, talk to us.

* Unit is a financial technology company and not a bank. Banking services are provided by Unit's partner banks, Members FDIC. Unit is not a lender. Merchant cash advances are purchases and sales of future receivables, not loans or extensions of credit. Lines of credit are loan products issued by Unit’s credit partner. Capital products are for business purposes only and are subject to underwriting requirements, terms, and conditions.

** Certain features, products, and activation tools described above may not be available for all programs and may depend on product configuration, bank approval, and eligibility requirements.

Frequently asked questions

What makes Unit different from other embedded finance providers?

Most infrastructure providers give you APIs and step back. Unit gives you the infrastructure and the activation layer on top of it. We've launched more than 100 embedded finance programs for software companies. That means we've seen where programs stall, and we've built the tools to address those gaps. Ready-to-Launch ships with pre-built marketing banners, lifecycle communications, onboarding flows, and post-approval checklists - you're not building activation from scratch.

Does Ready-to-Launch limit how we can build or customize later?

No. Ready-to-Launch and Custom are two ends of the same implementation spectrum, running on the same infrastructure. Platforms that launch on Ready-to-Launch can expand their use case, adjust their UX, or deepen their integration over time without replatforming. You're choosing an implementation approach, not locking into a tier.

Where can I learn more about Ready-to-Launch?

Check out the Ready-to-Launch page, and explore the technical docs for Ready-to-Launch Banking, Capital and Bill Pay. You can also read how RentSpree built a dedicated financial platform for landlords using Ready-to-Launch.