How to offer your customers debit, credit, and charge cards

Cards create value for your customers and drive revenue for your company. Learn how the different card types work and how to create a card program in weeks.

Card use continues to rise

According to the Federal Reserve Bank of San Francisco, cards are now the most-used payment option in the United States.

To be precise, debit, credit, and charge cards now account for more than 57% of all US payments by volume—and that number continues to rise.

That’s just one of the reasons that leading tech companies (e.g., Uber, DoorDash, Square) have started making branded payment cards available to their customers.

Cards are a convenient way to spend money, and they often generate rewards. In the case of credit and charge cards, they enable access to funds your customers don’t currently have in their bank accounts. Finally, businesses can manage corporate cards as a way to control spend.

But cards aren’t just valuable for your customers. They generate game-changing, new revenue streams in the form of interchange fees. They also drive engagement and retention, while generating valuable insights into customer cash flow and spending patterns.

If you’re a leader at a tech company who’s thinking about whether offering branded cards makes sense and how to offer them, this guide is for you. In it, we’ll cover:

- The value of cards for your customers

- The benefit of offering branded cards for your platform (revenue, data, and retention)

- The different kinds of cards (debit, credit, and charge)

- How to combine cards with other financial products

- How to launch a card program

The value of cards for platforms

Your customers are going to spend money. So why not help them do it in a way that’s convenient and rewarding for them—and also valuable for you?

To illustrate, let’s use an example. Say you’re the VP of Product at Kabin, a marketplace for vacation rentals. One of your hosts uses their Kabin Balance debit card to purchase $200 worth of painting supplies at the Home Depot.

For starters, you’ll earn $3 of interchange revenue from that transaction. At the same time, you’ll gain valuable insights into your host’s cash flow and spending patterns. Finally, you’re more likely to retain them, as they’re using your platform to store and spend their money.

When your customers spend money with your cards, they generate:

- Revenue. When your customers make card purchases, you earn a percentage of each transaction. This is known as interchange revenue, and for many tech companies, it’s a game changer. For example, Expensify is able to offer a free product for small businesses financed through interchange. Additionally, if you’re offering credit cards, you can earn financing revenues.

- Data. Offering your customers cards is a great way to understand their cash flow and how they’re spending their money. You can use this knowledge to tailor your product to their needs and make targeted offers. (You can also use it to underwrite additional lending and financing products.)

- Engagement and retention. When customers use your card to pay, they end up engaging more with your platform—to check their balances, pay their bills, and redeem rewards. They’re also less likely to churn. For example, customers who bank with Roofstock are retained 3.5x more than non-banking customers, and they log in twice as much.

It’s worth noting that people actually spend more when they pay with cards vs. cash. The average value of a cash transaction in the United States is $22—but that number rises to $43 for debit cards and $96 for credit cards. These are meaningful differences, especially when you consider the interchange revenue that cards generate for companies that offer them.

Understanding the different card types

Broadly speaking, there are three types of payment cards: debit cards, charge cards, and credit cards. Which you choose to offer will depend on your customers and your goals.

- Debit cards. Debit cards enable your customers to spend the money they have in their bank accounts. They’re typically easier to launch than credit or charge cards and can be a great on-ramp to other financial products—while still generating robust engagement, retention, and revenue.

- Charge cards. A charge card enables your customer to make purchases with a line of credit. They’re different from other credit cards in that your customers must pay down the full balance each repayment period (typically monthly). This reduces your exposure to nonpayment risk while helping your customers build a credit history.

- Credit cards. Unlike charge cards, credit cards can carry a revolving balance, meaning your customers don’t have to pay down the entire amount each month. Credit cards generate higher interchange than debit cards; however, they also carry the risk of nonpayment.

What can you offer with cards?

Cards are one of the most valuable financial products you can offer; they provide a powerful way for customers to make purchases and access funds, while providing you revenue.

But, when combined with other financial products, they can be a force multiplier that produces even better financial solutions and outcomes for your business. For example, they can enable you to offer instant payouts or free invoice factoring.

In this section, we’ll explore some of the ways innovative tech companies are combining cards with other financial products to generate engagement, retention, and revenue.

A convenient way for customers to spend money

Who’s doing it: Square, Invoice2go

How it works: The most basic use case for debit cards. Your customers use their cards to make purchases at the point of sale, either online, in person, or over the phone.

Benefits for your platform: You earn interchange revenue when your customers make card purchases.

Financial products:

- Debit cards

- Checking accounts

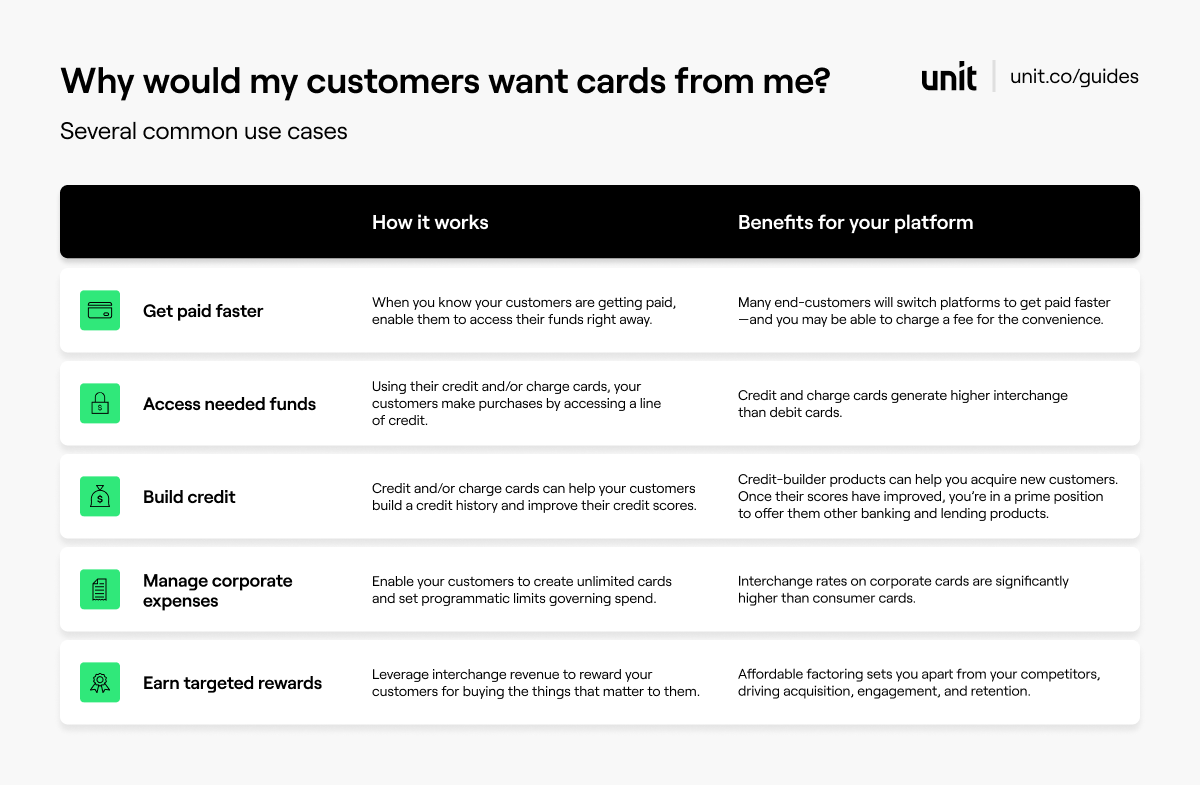

Help your customers get paid faster

Who’s doing it: DoorDash, Veryable

How it works: When you know your customers are getting paid, enable them to access their funds right away.

Benefits for your platform: Many end-customers will switch platforms to get paid faster—and you may be able to charge a fee for the convenience.

Financial products

- Debit cards

- Checking accounts

- Instant payouts

Help your customers access needed funds

Who’s doing it: Amazon, eBay

How it works: The most basic use case for credit and charge cards. Your customers can make purchases with a line of credit.

Benefits for your platform: Credit and charge cards generate higher interchange than debit cards.

Financial products

- Credit or charge cards

Help your customers build credit

Who’s doing it: Chime, Nav

How it works: Credit and/or charge cards can help your customers build a credit history.

Benefits for your platform: Credit-builder cards can help you acquire new customers. Once their scores have improved, you're in a prime position to offer them other banking and lending products.

Financial products

- Credit or charge cards

- Checking accounts

Help your customers manage corporate expenses

Who’s doing it: Ramp, Highbeam

How it works: Enable your customers to set programmatic limits governing card spend (e.g., amounts, merchant categories).

Benefits for your platform: Interchange rates on corporate cards are significantly higher than consumer cards.

Financial products

- Credit or charge cards

- Checking accounts

Offer industry-leading factoring rates

Who’s doing it: Outgo, Creative Juice

How it works: Leverage interchange revenue to lower the cost of invoice factoring for your customers.

In this case, whether you choose debit, credit, or charge cards will influence both the functionality of your product and the factoring rates you can offer.

For example, you could choose to subsidize factoring fees from debit card purchases or provide free factoring from charge card purchases. Also, with a credit or charge card, your customers don’t need to wait for an invoice to be factored before they start spending.

Benefits for your platform: Affordable factoring sets you apart from competitors—driving acquisition, engagement, and retention.

Financial products

- Debit, credit, or charge cards

- Checking accounts

- Factoring

Offer targeted rewards

Who’s doing it: Paypal, Bluedot

How it works: Leverage interchange revenue to reward your customers for buying the things that matter to them.

Benefits for your platform: Targeted rewards set you apart from competitors—driving acquisition, engagement, and retention.

Financial products

- Debit, credit, or charge cards

- Bank accounts

How cards enable you to offer credit to your customers

Underwriting and capital

One of the most important differences between card types is whether they require underwriting and operational capital.

Because debit cards draw funds from your customers’ bank accounts, they don’t require either.

By contrast, credit and charge cards draw funds from money lent to your customers. As such, they require underwriting. That means determining whether and how much credit to extend each customer.

Funding your credit- and/or charge-card program will require sourcing the necessary operational capital (Unit can help with this). It typically comes from one of three places:

- Your balance sheet. For newer programs, this is often the most simple option. Once you’ve established a successful lending program, you can typically add a capital partner if you desire.

- Your bank partner. In some cases, your bank partner may be willing to act as the lender for the credit- and/or charge-card program. However, your bank will typically need to be compensated for access to their capital and assuming any associated credit risk.

- A third-party provider. You can also partner with an independent capital provider. As with banks, they typically charge a fee for access to their capital.

How Unit can help

Unit is a modern financial infrastructure platform that helps tech companies build accounts, cards, payments, and lending into their products.

That means we help platforms like yours launch payment cards (among other things). To date, nearly 200 leading platforms and marketplaces have trusted us to help them build and scale their card programs.

For example, Unit helped AngelList add bank accounts and debit cards to their platform, thereby becoming a “financial mission control” for their customers.

If you’re ready to launch your card program, we can help with the following:

- Bank partner(s). We work with multiple bank partners to ensure reliability and offer the most complete product set. We also help you understand your obligations and manage the relationship(s).

- Compliance. Unit streamlines compliance, helping with things like KYC, transaction monitoring, and manual account reviews. That way, you can focus on your customers.

- Technology. We’ve built all the necessary banking and lending infrastructure—so you don’t have to. Using our white-label UIs, tech companies can seamlessly embed cards into their apps with a few lines of code.

- Program management. Offering payment cards means establishing relationships with card printers, card networks, payment processors, ATM networks, and issuing banks—just to name a few. Doing it on your own will require full-time staff and months of work. Fortunately, Unit takes care of it for you. All you have to do is design your cards (and we can help with that too).

- Underwriting. Underwriting means figuring out whom to lend to, how much, and on what terms. It’s a complicated process, and traditional banks take a one-size-fits-all approach. When you work with Unit to make credit and charge cards available to your customers, we facilitate an underwriting process with your bank and make it simple to leverage proprietary data to offer more tailored solutions.

- Capital. Of course, you can provide the funds to your customers from your balance sheet—but this might not be the best use of your money. As an alternative, Unit can provide access to capital; in exchange for a fee, we can streamline funding your customers’ credit- and/or charge-card purchases.

If you’ve got questions about cards, please reach out; we’d love to brainstorm with you. Alternatively, you can check out our sandbox and start building now.

Frequently asked questions

Can Unit help me launch a branded debit card program?

Yes, we can help you launch a branded debit card program.

Once you’re a Unit customer with production access, you just make an API call. We’ve already optimized the relationship between the bank, processor, and network, removing much of the complexity and manual labor you would have had to go through to set up a program.

Credit vs charge cards: what’s the difference?

A charge card is a type of credit card. It allows your customers to pay with a revolving line of credit, right at the point of sale.

Unlike credit cards, charge cards can’t carry a revolving balance. In fact, they must be paid off completely at the end of every statement period (typically monthly). Because of that, charge card holders don’t pay interest on their cards.

Charge cards also impact credit scores differently. Notably, they don’t have a preset spending limit; this means that credit scoring models can’t calculate your customer’s ratio of available credit to amount spent (known as their credit utilization score). Your customer could spend as much as they wanted in a given month with a charge card—and it won’t be reflected in their utilization score.

What is the fastest way to launch a card program?

Launching a card program is easy, and can be done within five weeks. Just submit your logo to us; we’ll take care of the rest.