A complete guide to embedded banking

Embedded banking enables tech companies to make a range of banking services available to their customers. Explore how it can add value to your company.

The rise of embedded banking

In a recent survey of leaders in global finance, more than 70% said they expect over half of financial services to be offered through nonfinancial platforms in the near future.

What does that mean, exactly? How are financial products making their way into apps like Uber and Shopify?

The answer is embedded banking. That’s when a tech company teams up with a financial institution to make banking products (e.g., high-yield accounts, credit cards) available inside their app or website.

One familiar example is Square Checking. Thanks to embedded banking, merchants who use Square’s point-of-sale (POS) solutions can also take advantage of Square bank accounts and debit cards. Among other advantages, this enables them to get paid within moments of completing a sale.

For Square, this has resulted in explosive revenue growth. In fact, in Q4 2022, Square’s gross profits from its merchant segment were up 22%, to $801M.

If you’re a leader at a tech company who’s curious about embedded banking, this guide is for you. In it, we’ll address questions like:

- How does embedded banking work?

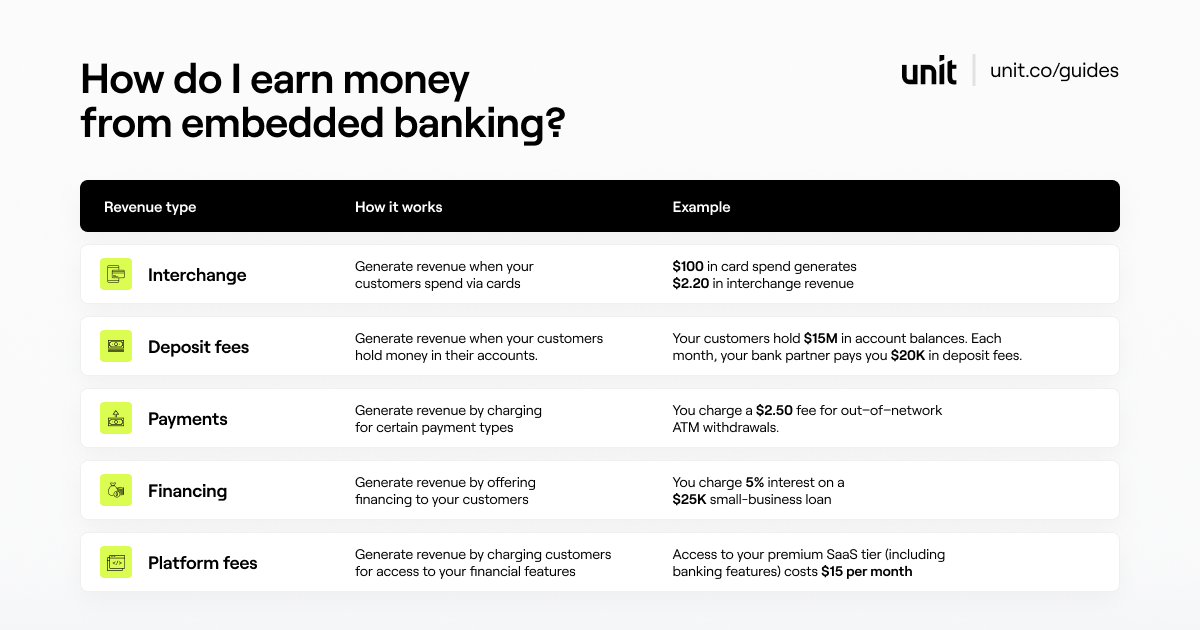

- How does it generate revenue?

- What kinds of companies are a good fit?

- Why would my customers want it?

- What does it take to launch?

What is embedded banking?

Embedded banking enables tech companies to make financial products (e.g., high-yield accounts, credit cards) available within their apps and websites.

Shopify Balance is a well-known example. Thanks to embedded banking, merchants who use Shopify to manage their ecommerce businesses can also take advantage of Shopify bank accounts and business loans. Among other advantages, this enables them to get paid within moments of completing a sale.

Embedded banking enables you to offer four kinds of financial products to your customers:

- Bank accounts. Embedded bank accounts work just like other bank accounts. Some can even generate interest for your customers.

- Debit, credit, and charge cards. Branded payment cards are a convenient way for your customers to spend money from their bank accounts (debit cards) and/or access needed funds (credit or charge cards). They can be created virtually or physically printed.

- Payments. Your customers want to move money: to do things like pay their rent, send remittances, and make peer-to-peer transfers. With embedded payment methods like ACH, wires, book transfers, and checks, you enable them to do so.

- Lending and financing. Embedded lending and financing involve giving your customers access to needed funds. Common forms include credit cards, charge cards, term loans, invoice factoring, and cash advances.

How embedded banking works

To show how embedded banking works, let’s use another real-world example: Lyft Direct.

In the Lyft app, drivers choose how they want to get paid. If they choose Lyft Direct, they can access their money within moments of completing a ride, right in their Lyft Direct bank account. They also receive a stylish debit card that earns cash back on things like gas and groceries.

Drivers love it not just because they can get paid right away, but also because they can manage their entire ride-share business (including accounting and taxes) from inside the Lyft app. For Lyft, the program is valuable because it generates several robust new revenue streams.

Behind the scenes, Lyft partners with Stride Bank to offer these financial products. Drivers interact with their bank accounts and debit cards via the Lyft app, and those requests are transmitted back and forth to Stride Bank, where the funds are held, via an application programming interface (API).

Many tech companies who offer embedded banking choose to do so with the help of a financial infrastructure platform. Such a partnership drastically reduces the required investment of time, money, and staffing. Working without one can take up to two years and $2 million, but a modern financial infrastructure platform can have you up and running in weeks.

Common use cases for embedded banking

A common question I hear from founders and product folks is “What kinds of companies are a good fit for embedded banking?”

There are two ways to answer this question. The first is, itself, a list of questions:

- Does your product have a large transaction volume? (e.g., Shopify)

- Do your customers have unique financial needs? (e.g., Baselane)

- Do you have a strong brand and a devoted customer base? (e.g., Square)

- Do you want to pay your customers faster? (e.g., Veryable)

- Are your customers underserved financially? (e.g., Lyft)

- Do your customers need access to capital? (e.g., Nav)

If you answered “yes” to any of the above, then you’re probably a good fit for embedded banking. There are also several use cases that work particularly well:

1. Gig-economy companies

Gig workers expect to be paid right away. In many cases, they’re accepting work opportunities today so they can pay their bills tomorrow. Embedded banking is a powerful way to offer instant payouts that functions as a revenue generator rather than a cost center.

2. E-commerce marketplaces

Marketplaces like Etsy and Shopify present a near-perfect use case for embedded banking. When they offer embedded banking, they provide their merchants with faster payouts and tailored financing options. They also keep more funds on their platform, boosting their bottom line.

3. Vertical SaaS companies

Your customers don’t want to manage their business operations and their business finances separately. When you offer embedded banking, you become “mission control,” enabling your customers to manage all aspects of their company from within your platform.

4. Payroll and employee benefits providers

Processing payroll? Many employees don’t have bank accounts, and many more would welcome the convenience of banking with their payroll provider (e.g., Gusto Wallet). The same principle applies to employee benefits like HSA and FSA accounts.

5. Business formation and management

Do you help small businesses incorporate? Draft proposals, send invoices, manage their websites? If so, you’re a great fit for embedded banking. Small-business owners want help managing their finances, and you’re in a great position to offer it.

Why customers choose embedded banking products

When it comes to financial products, Americans have a lot of options—so it’s natural to wonder why they would choose yours.

The short answer is that a majority of American small businesses are dissatisfied with the way they manage their money today—and they’re eager for an alternative. In fact, 84% of small businesses we surveyed said they would explore financial products from their business software tool, if they were offered.

For your customers, embedded banking products offer four distinct advantages.

- Faster access to funds. Embedded banking helps you pay your customers faster—even on demand. It’s a way of offering instant payouts that generates revenue rather than costing you money.

- Better financing options. 62% of businesses we surveyed said they can’t get the lending and financing they need. Fortunately, you’re in a great position to help. You understand your customers’ business models and their cash flow; you know what they need and how much they can afford to repay.

- More tailored terms. Traditional financial institutions weren’t built to serve the needs of small businesses—and they haven’t kept up with the times. When you offer embedded banking, you can provide more tailored terms: fewer fees, better interest rates, and targeted rewards for the things your customers care about.

- A one-stop shop. According to Baselane founder Mathias Korder, “Banking is the source of truth for any small business.” Adding banking to your product transforms you into a one-stop shop: a single software tool that your customers can use to manage every aspect of their companies.

How embedded banking benefits tech companies

Embedded banking products don’t just create value for your customers; they enable you to capture more value.

- Product differentiation. With embedded banking, you offer a more complete product and a better user experience. As a result, you stand out from competitors. For example, Roofstock has seen a 4x higher customer lifetime value when customers use Stessa Cash Management accounts.

- Acquisition. A differentiated product makes it easier to acquire customers—and correspondingly lowers your acquisition costs. For example, after they launched embedded banking, Baselane saw their customer acquisition cost decrease by 50%.

- Engagement. When you make banking services available, your customers engage more with you more—for things like payments, accounting, and financial insights. For example, customers who use Nav’s embedded bank accounts are 2.5x more likely than non-banking customers to pay for additional Nav products (e.g., apply for a loan, purchase a detailed credit report).

- Retention. Banking is famously sticky. For example, Roofstock found that customers who use their Stessa Cash Management accounts are retained at a rate 3.5x higher.

- Satisfaction. A more complete product leads to greater satisfaction. For example, customers who use Nav’s embedded bank accounts have an NPS of 79, 35% higher than non-banking customers.

- Revenue. Ultimately, the items in this list lead to increased revenue generation. In fact, embedded banking has the potential to generate five distinct revenue streams, and can lead to 2-5x increase in revenue per user. To get a detailed estimate of what you could be earning, check out our revenue calculator.

What does it take to launch embedded banking?

In other words, what will you need to invest in terms of time, money, and staffing? The answer varies widely depending on your approach.

For example, it’s possible to do from the ground up, as many early banking apps did (e.g., Chime, Current). However, this approach can take 2 years and $2 million to launch, and it will require hiring a large, dedicated banking team.

On the other hand, you could partner with a bank using a financial infrastructure platform. The advantage of this approach is that you can usually go live in a matter of weeks. They’ll typically support things like:

- Direct bank relationship. There are more than 4000 banks in the United States, but only a few dozen have demonstrated the ability to effectively partner with tech companies to offer embedded banking. A good financial infrastructure platform will help you identify a bank partner that specializes in your target audience and use case.

- Technology. Embedded banking requires dedicated software to perform tasks like ledgering, payments, and reconciliation. It’s complex, and the stakes couldn’t be higher. Choose a partner with a proven track record of success who can provide all the necessary banking technology.

- Compliance. Banking is subject to dozens of compliance and regulatory requirements—most of which will be unfamiliar to non-experts. Your embedded-banking provider should have a team of experienced compliance professionals to help guide you.

- Underwriting. Underwriting means figuring out whom to lend to, how much, and on what terms. It’s hard to get right, and mistakes can be costly. Fortunately, a financial infrastructure platform can facilitate underwriting and make the process simple.

- Capital. Lending to your customers requires operational capital—the funds you’ll advance, which will later be repaid. Many tech companies prefer not to leverage funds from their balance sheet for this purpose. For this reason, several financial infrastructure platforms also provide access to the capital needed to fund lending programs.

How Unit can help

Unit is a financial infrastructure platform for software companies that want to store, move, spend, and lend money inside their products. The platform also offers tooling to run your financial products, as well as managed operations you can delegate to Unit. Configure your build with the elements you need and the level of ownership you want, including a managed solution: a pre-configured build that Unit runs for you and you embed in one line of code.

If you’re thinking about how embedded banking can add value to your platform, please reach out. We’d love to brainstorm with you.

Frequently asked questions

Is white label banking safe?

White label banking is generally safe and secure, thanks to the stringent regulatory requirements that apply to financial institutions and the robust security measures they employ.

The safety of white label banking services is underpinned by several key factors:

- Regulatory compliance. White label banking services are offered through established financial institutions that are required to comply with all relevant regulations.

- Data encryption. Data transferred between the user, the platform, and the banking partner is encrypted to prevent unauthorized access.

- Fraud detection. Advanced fraud detection systems are employed to monitor transactions and identify suspicious activity.

- Privacy policies. Rigorous privacy policies ensure that customer data is protected and used in compliance with data protection laws.

- Insurance. Funds held in white label banking accounts are often insured by the government. In the United States, for instance, FDIC insurance covers up to $250,000 per depositor.

What is a neobank?

A neobank is a company that offers online banking services without physical retail locations (“bank branches”) that a customer can visit.

A few neobanks (e.g., Varo, SoFi) hold bank charters, but most do not. The rest offer banking services via white label banking (e.g., Mercury, BlueVine).

Many neobanks focus on improving the user experience. They offer features such as real-time notifications, instant payments, budgeting tools, savings goals, and easy-to-use interfaces.

How does embedded banking relate to the concept of open banking?

The two concepts are complementary; both represent the next stage in the evolution of financial services.

Open banking enables businesses and consumers to digitally connect their bank accounts (and other financial data) to third-party apps and services. For example, when you link your bank account to Venmo or Cash App, that’s open banking.

Embedded banking enables tech companies like Uber and Shopify to make banking services (e.g., bank accounts, credit cards) available inside their apps and websites.

What is the difference between embedded banking and embedded finance?

Embedded banking is a subset of embedded finance.

Embedded banking refers to the integration of banking services, such as payments, lending, and account management, directly into non-financial platforms.

Embedded finance is a broader concept encompassing a wide range of services, including embedded insurance, investments, and financial planning.

What is the difference between digital wallets and white label banking?

Digital wallets are apps that store payment information, enabling users to make electronic transactions.

They can hold credit/debit card details, bank account information, and digital currencies. Well-known examples include Apple Wallet and Google Wallet.

White label bank accounts are typically comprehensive bank accounts, with features like check deposits, wire transfers, and access to other financial products. They are offered by a regulated financial institution and sold under the logo of another company. For example, Shopify Balance and Uber Pro Card include white label bank accounts.

White label bank accounts come with several advantages over digital wallets. These accounts typically offer a broader range of services and are often eligible for FDIC pass-through insurance coverage. Unlike most digital wallets, they can potentially earn interest for the account holder.

What’s the difference between white label banking and private label banking?

White label banking and private label banking are two terms that refer to different types of partnerships between banks and non-bank entities.

- In a white label banking arrangement, a non-bank entity offers banking products or services to its customers under its own brand name. Still, the products or services are actually provided by a licensed bank behind the scenes.

- In a private label banking arrangement, a licensed bank offers banking products or services to a specific group of customers under a different brand name than its own. The bank may partner with a non-bank entity that has access to the target customer group, such as a retailer or an airline.